People are sort of expecting this to happen but this was simply too sudden! Given that the Ascendas-Singbridge acquisition just completed a few days ago?! Anyway, I am not sure why they are calling it a combination instead of a merger but I guess it is because they already owned it?

What is Happening?

Ascott REIT shareholders:

Nothing to get too excited about.

Ascendas Hospitality Trust shareholders:

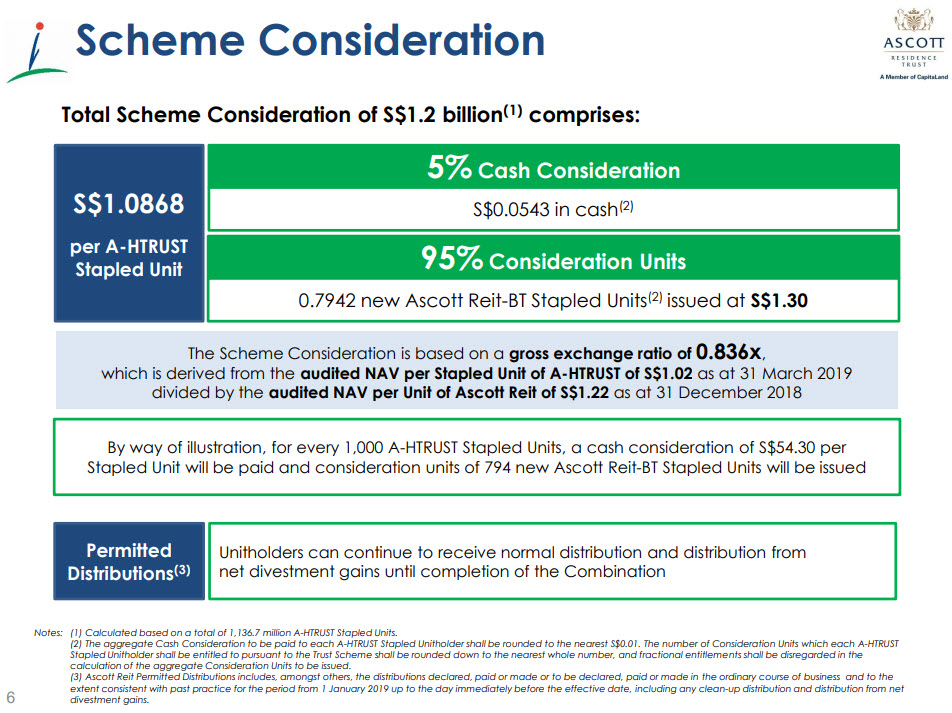

Ascott REIT will be buying over your shares! This will comes in the form of $0.0543 cash/dividends + 0.7942 of new Ascott REIT-BT shares. Value unlocked? It really depends on how one looks at it.

Let's look back at one of our posts where I blogged about the open letter by Quarz Capital in our Portfolio - April 2019 and decided to buy more Ascott REIT.

As you can see, the offer is pretty similar to what Quarz Capital proposed - a mixture of cash (lesser) and Ascott REIT share (more) offer at a 5-10% premium to book value. In my opinion, the offer is quite fair and it does unlock the value for Ascendas Hospitality Trust. The next question will be is this better for Ascott REIT and/or Ascendas Hospitality Trust shareholder?

NAV and DPU

During such event (acquisition/merger), they will always market that it is good for the shareholders but it is not always the case e.g. Another Bad Deal - Merger of OUE Commercial REIT & OUE Hospitality Trust. One glance on the presentation slides or newspaper article will reveal that DPU will improve for both Ascott REIT and Ascendas Hospitality Trust shareholders.

With more assets and "better" branding, it should be expected/normal for the new entity to trade at higher PB. Unfortunately, the dividend yield actually decreases for Ascendas Hospitality Trust shareholders. The dividend yield increases for Ascott REIT shareholders. On a side note, the pro forma NAV should have been $1.21, decrease by $0.01 including all the fees/costs but I found it amusing that they only stated that in the fine print and marketed it as DPU accretion, NAV neutral. lol.

Arbitrage Opportunity

Based on the latest closing price of both shares on 3rd July 2019, buying Ascendas Hospitality Trust still provides an estimated 2.96% return (before fees/commissions and higher return if annualized). Technically, both prices should be "supported" by this combination - Ascott REIT ~$1.30 and Ascendas Hospitality Trust ~$1.08. So whenever Ascott REIT price is > $1.30 or Ascendas Hospitality Trust price is < $1.08 are buying opportunities...

Having said that, nothing is stopping Trump from pulling any stunt that will lead to the whole market turning red again. In addition, with both stock prices at an all-time high, the chances of them falling is definitely much higher.

Indicative Timeline

Simply buying Ascendas Hospitality Trust when it is below $1.08. What's the risk? If you look at the indicative timeline, you will know that it is not happening immediately and has to be voted by the shareholders during the October 2019 EGM. There is a possibility of it not happening. Imagine market sentiment turns weak and Ascott REIT price falls to $1.10 (back in December 2018). The combination/merger will be an immediate loss for Ascendas Hospitality Trust shareholders!

Odd Lots

If you are wondering if there is any way NOT to end up with odd lots, the answer is going to disappoint you. You will almost definitely end up with odd lots but you can definitely try to end up with the least odd lots. A realistic example - if you have 3000 Ascendas Hospitality Trust shares now, you can buy 400 more shares so that you will be given 2700 Ascott REIT shares. This will only make sense if you have no minimum commission. Otherwise, you will be better off with odd lots.

I would have preferred more cash to be paid out vs getting new Ascott REIT shares at $1.30. Oh well, we are sitting on decent profits for both stocks so not going to complain further. So will you buy or bye?

You can find the spreadsheet here:

- Combination of Ascott REIT and Ascendas Hospitality Trust Calculator

You can refer to the official announcements here:

- Ascott REIT Announcements

- Presentation Slides

Do like any of the following for the latest update/post!

1. FB Page - KPO and CZM

2. Twitter - KPO and CZM

3. Click here to subscribe using email :)

4. Instagram - KPO_and_CZM (Did you see those delicious food photos to the right --> Unfortunately, you can't see it on mobile.)

What is Happening?

Ascott REIT shareholders:

Nothing to get too excited about.

Ascendas Hospitality Trust shareholders:

Ascott REIT will be buying over your shares! This will comes in the form of $0.0543 cash/dividends + 0.7942 of new Ascott REIT-BT shares. Value unlocked? It really depends on how one looks at it.

Let's look back at one of our posts where I blogged about the open letter by Quarz Capital in our Portfolio - April 2019 and decided to buy more Ascott REIT.

As you can see, the offer is pretty similar to what Quarz Capital proposed - a mixture of cash (lesser) and Ascott REIT share (more) offer at a 5-10% premium to book value. In my opinion, the offer is quite fair and it does unlock the value for Ascendas Hospitality Trust. The next question will be is this better for Ascott REIT and/or Ascendas Hospitality Trust shareholder?

NAV and DPU

During such event (acquisition/merger), they will always market that it is good for the shareholders but it is not always the case e.g. Another Bad Deal - Merger of OUE Commercial REIT & OUE Hospitality Trust. One glance on the presentation slides or newspaper article will reveal that DPU will improve for both Ascott REIT and Ascendas Hospitality Trust shareholders.

|

| Based on the closing price on 2nd July before the announcement |

With more assets and "better" branding, it should be expected/normal for the new entity to trade at higher PB. Unfortunately, the dividend yield actually decreases for Ascendas Hospitality Trust shareholders. The dividend yield increases for Ascott REIT shareholders. On a side note, the pro forma NAV should have been $1.21, decrease by $0.01 including all the fees/costs but I found it amusing that they only stated that in the fine print and marketed it as DPU accretion, NAV neutral. lol.

Arbitrage Opportunity

Based on the latest closing price of both shares on 3rd July 2019, buying Ascendas Hospitality Trust still provides an estimated 2.96% return (before fees/commissions and higher return if annualized). Technically, both prices should be "supported" by this combination - Ascott REIT ~$1.30 and Ascendas Hospitality Trust ~$1.08. So whenever Ascott REIT price is > $1.30 or Ascendas Hospitality Trust price is < $1.08 are buying opportunities...

Having said that, nothing is stopping Trump from pulling any stunt that will lead to the whole market turning red again. In addition, with both stock prices at an all-time high, the chances of them falling is definitely much higher.

Indicative Timeline

Simply buying Ascendas Hospitality Trust when it is below $1.08. What's the risk? If you look at the indicative timeline, you will know that it is not happening immediately and has to be voted by the shareholders during the October 2019 EGM. There is a possibility of it not happening. Imagine market sentiment turns weak and Ascott REIT price falls to $1.10 (back in December 2018). The combination/merger will be an immediate loss for Ascendas Hospitality Trust shareholders!

Odd Lots

If you are wondering if there is any way NOT to end up with odd lots, the answer is going to disappoint you. You will almost definitely end up with odd lots but you can definitely try to end up with the least odd lots. A realistic example - if you have 3000 Ascendas Hospitality Trust shares now, you can buy 400 more shares so that you will be given 2700 Ascott REIT shares. This will only make sense if you have no minimum commission. Otherwise, you will be better off with odd lots.

I would have preferred more cash to be paid out vs getting new Ascott REIT shares at $1.30. Oh well, we are sitting on decent profits for both stocks so not going to complain further. So will you buy or bye?

You can find the spreadsheet here:

- Combination of Ascott REIT and Ascendas Hospitality Trust Calculator

You can refer to the official announcements here:

- Ascott REIT Announcements

- Presentation Slides

Do like any of the following for the latest update/post!

1. FB Page - KPO and CZM

2. Twitter - KPO and CZM

3. Click here to subscribe using email :)

4. Instagram - KPO_and_CZM (Did you see those delicious food photos to the right --> Unfortunately, you can't see it on mobile.)

Most investors in AHT would prefer cash or something more straight forward. I am not a finance person and have a feeling that it only benefit CapitaLand and Ascott. This kind of stupid scheme will end up with odd lots for retail investors that we cannot see without a "huge" cost at the OTC. I will vote against this during the EGM.

ReplyDeleteHi Henry,

DeleteHonestly, I really don't think this is such a bad deal (I have seen worst). Besides, AHT has never traded close to its NAV or at such high level and this deal has unlocked its value.

I see. If the odd lots really affect you, you can consider selling it off after the EGM because I think this will most likely go through...

Hi KPO, I see this stock as a good passive income which I get about 8.5% yield. Where to find such a high yield good company. I am happy to hold it forever even without price appreciation. Am not sure how to get the same yield after the merger? Also unsure how to rationalise this from a dividend yield perspective if this deal is really good for me. Any advise from you will be good.

DeleteRP gave an excellent reply below. You are looking at yield on cost.

DeleteExample,

You have 1000 AHT shares at 70.9 cents

DPU 6.03 cents ---> ~8.5% yield on cost.

After the deal,

You will get 794 ACT shares + $54.30 cash/dividends.

Your cost for AHT is 1000 * $0.709 = $709

Your "cost" for ACT will be ($709 - $54.30) / 794 ~ $0.825

DPU 7.34 cents ---> 8.90% yield on cost. Not bad right?

Hope this is clearer...

@henry

ReplyDeleteWhether to view yield as yield on cost or market price is the question.

Although it is "nice" to look at the high yield on cost, which in your case is 8.5%, more realistically you should look at the yield on market price, which is currently 6.2%.

This gives a better indication whether to hold or sell and buy another counter with a higher yield.

After the merger you could, I suppose, continue to calculate your yield based on the original cost of the AHT units, and you would end up with about 8% or so.

Note that you will also be receiving some cash, which you can either regard as capital return and reduce the cost of your units accordingly, or as dividend income which will give a short term boost to the yield.

In summary I think it is useful to look at both yields, but yield on market price is the one to use for sell/buy decisions.....

Hi, May I know how you calculate for potential loss 1.54% for Ascott BT unit? Thank you.

ReplyDelete