Blogging is a way for us to share with our readers our plan/strategy towards our financial freedom. The thing is there are just so many things we do not know as well and occasionally readers will reach out and share their knowledge with us. After my last article on 1% Net Worth to Crypto which I thought xfers was the most cost-effective way to buy crypto and that the transfer fees are too high, a reader reached out and shared with me that I can wire USD directly to BlockFi and make use of their free transfer/withdrawal (one free crypto withdrawal per calendar month and one free stablecoin withdrawal per month) to avoid the transfer fees. Besides that, he also introduced Celsius Network and DeFi to me. Personally, I found DeFi to be more complicated/troublesome so I did not read up/research further but I was attracted to Celsius Network.

What are BlockFi and Celsius Network?

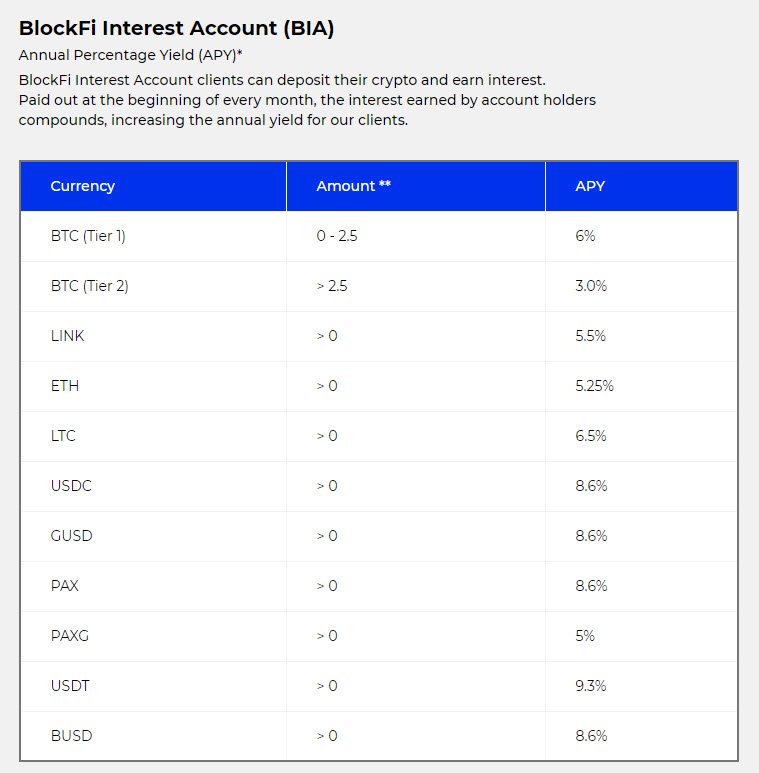

They are simply your crypto savings account (similar to your bank account) where interests are given on a monthly/weekly basis.

In my opinion, use BlockFi for the non-stablecoins like BTC and ETH.

How can they pay such high interest?

In layman's term, they are functioning like a bank, lending out our deposits for higher interest but instead of keeping the majority to themselves as profits, they are sharing more of it with us. Take a look at these articles from Celsius Network:

- Celsius Network Interest Rates, ExplainedAnyway, after reading up the FAQs on BlockFi, I went ahead to test it out using the minimum amount required ($10 USD) to wire/transfer based on the instruction provided. Besides getting the SWIFT code right, you must remember to add your 8-digit PIN in the notes/comment section under "Other Details".

It took about a day for the transfer to show up in my BlockFi account with a 1:1 conversion to GUSD which is a 1:1 USD-backed stablecoin by Gemini. No fees at all!

With that, my USD is now earning 8.6% interest, paid out on a monthly basis for BlockFi. Once I confirmed that my capital is not being "eaten" up by any fees, I proceeded to transfer a larger amount ($1k USD) to BlockFi. Tip: Initiate the wire transfer over the weekdays for it to be cleared/reflected faster. I did it on a Saturday and it was only reflected on Monday.

This brings me to Celsius Network. I initiated a withdrawal of $200 USD from BlockFi to Celsius Network. It took more than a day because of a 1-day security hold feature implemented by BlockFi. Since the withdrawal is processed the next business day after the security hold is over, it can be cancelled for whatever reason (e.g. wrong wallet address, change your mind, etc.).

Now the full $200 USD is in my Celsius account earning 10.51% interest! With this, I have completed my testing and will be pumping more money (~20-30k USD) into Celsius since there are no fees involved. Shall provide another update once I move them over and received some interests :)

What are the risks?

You can read a more in-depth review from CoinCentral but I have extracted the relevant section below:

What happens if BlockFi gets hacked?: “Gemini is BlockFi’s primary custodian and BlockFi doesn’t hold private keys directly. Gemini keeps the vast majority of its assets in cold storage and is insured by Aon. Gemini is a licensed custodian and regulated by the NYDFS. They recently received SOC2 Type 1 compliance audit from Deloitte for their custody solution. We encourage users to read more about Gemini’s security. “

What happens if a user account is compromised?: “Since inception, BlockFi has not lost any customer funds. In the event that a user’s account is compromised, which our security protocols have caught in the past, we freeze the individual’s account for one week. Then, we conduct a Videoconference with the affected individual to verify their identity. We can then change their email address and password, so they can regain control of their account.”

What happens if suddenly everyone defaults on their cryptocurrency loans?: “When we lend crypto assets to generate yield, we have an extremely thorough risk management and credit analysis process. We only primarily lend to large, well-capitalized, institutional borrowers, or to counter-parties willing to post collateral and provide the ability to margin call them on a 24/7 basis.”

“What that means is, if we are lending $1M worth of BTC to Firm XYZ, Firm XYZ collateralizes the loan (typically ~120%) by giving us ~$1.2M USD. If the loan were to then enter margin call and the borrower was unable to provide additional collateral (default), we would use their USD collateral to buy crypto.”

“We have actively lent since January of 2018, including throughout multiple periods of high volatility, without any losses across our entire lending portfolio. BlockFi is bound by NDA’s to discuss terms of specific borrowers/rates.”

What happens if BlockFi gets hacked?: “Gemini is BlockFi’s primary custodian and BlockFi doesn’t hold private keys directly. Gemini keeps the vast majority of its assets in cold storage and is insured by Aon. Gemini is a licensed custodian and regulated by the NYDFS. They recently received SOC2 Type 1 compliance audit from Deloitte for their custody solution. We encourage users to read more about Gemini’s security. “

What happens if a user account is compromised?: “Since inception, BlockFi has not lost any customer funds. In the event that a user’s account is compromised, which our security protocols have caught in the past, we freeze the individual’s account for one week. Then, we conduct a Videoconference with the affected individual to verify their identity. We can then change their email address and password, so they can regain control of their account.”

What happens if suddenly everyone defaults on their cryptocurrency loans?: “When we lend crypto assets to generate yield, we have an extremely thorough risk management and credit analysis process. We only primarily lend to large, well-capitalized, institutional borrowers, or to counter-parties willing to post collateral and provide the ability to margin call them on a 24/7 basis.”

“What that means is, if we are lending $1M worth of BTC to Firm XYZ, Firm XYZ collateralizes the loan (typically ~120%) by giving us ~$1.2M USD. If the loan were to then enter margin call and the borrower was unable to provide additional collateral (default), we would use their USD collateral to buy crypto.”

“We have actively lent since January of 2018, including throughout multiple periods of high volatility, without any losses across our entire lending portfolio. BlockFi is bound by NDA’s to discuss terms of specific borrowers/rates.”

Given that both BlockFi and Celsius Network have been operating for ~3 years, they are unlikely to pull an exit scam too. In my opinion, the greatest risk is myself. Imagine if I fat finger/blur blur go transfer the crypto/money to a wrong wallet/address. It will simply disappear/vanish into thin air.

Summary

For BTC and ETH: Bank --wire transfer (no fee)--> BlockFi (interest ~5-6%)

For USD stablecoins: Bank --wire transfer (no fee)--> BlockFi --transfer (no fee)--> Celsius Network (interest ~10.5%)

If you are interested in the platform I am using, do sign up using our referral links for some bonus :)

BlockFi: Deposits US$100 or more into your BlockFi Interest Account (BIA), you will earn US$10 in BTC and we will earn US$10 in BTC too.

Celsius Network: Earn US$40 in BTC with your first transfer of US$400 or more and we will earn US$40 in BTC too.

Gemini: We will both receive US$10 of bitcoin after you buy or sell US$100.

Do like any of the following for the latest update/post!

1. FB Page - KPO and CZM

2. Twitter - KPO and CZM

3. Click here to subscribe using email :)

4. Instagram - KPO_and_CZM (Did you see those delicious food photos to the right --> Unfortunately, you can't see it on mobile.)

You might be interested in these articles too:

Do like any of the following for the latest update/post!

1. FB Page - KPO and CZM

2. Twitter - KPO and CZM

3. Click here to subscribe using email :)

4. Instagram - KPO_and_CZM (Did you see those delicious food photos to the right --> Unfortunately, you can't see it on mobile.)