An announcement was recently made on the merger of OUE Commercial REIT and OUE Hospitality Trust. I took a look and realized how the merger is a bad deal for both the existing shareholders. In addition, this happened after the OUE Commercial REIT rights issue less than a year ago - OUE Commercial REIT Rights Issue - Very Very Very Bad Deal which meant a double blow for OUE Commercial REIT shareholders.

OUE Hospitality Trust shareholders will be receiving $0.04075 cash + 1.3583 new OUE Commercial REIT shares for every existing OUE Hospitality Trust share. Let's look at the numbers to see why I deemed it as a bad deal.

OUE Hospitality Trust (Before Merger)

Last Close: $0.735

NAV: $0.75

PB: 0.980

DPU: 0.0499

Dividend Yield: 6.79%

OUE Commercial REIT (Before Merger)

Last Close: $0.52

NAV: $0.71

PB: 0.732

DPU: 0.0348

Dividend Yield: 6.69%

After Merger

You can see that the pro forma numbers are based on the issue price of $0.57 per new OUE Commercial REIT share.

Issue Price: $0.57

NAV: $0.62

PB: 0.919

DPU: 0.0348

Dividend Yield: 6.11%

What this means for OUE Hospitality Trust shareholders:

- The "buyout" is at below book value/NAV

- You got diluted/the dividend yield drops for the "same" investment

What this means for OUE Commercial REIT shareholders:

- You got diluted big time as the NAV decreases by ~12.7%

- The pro forma DPU shows an increase of 0.0341 to 0.0348 but 0.0341 is not the actual DPU for FY 2018. Unable to determine if it is truly yield accretive as stated

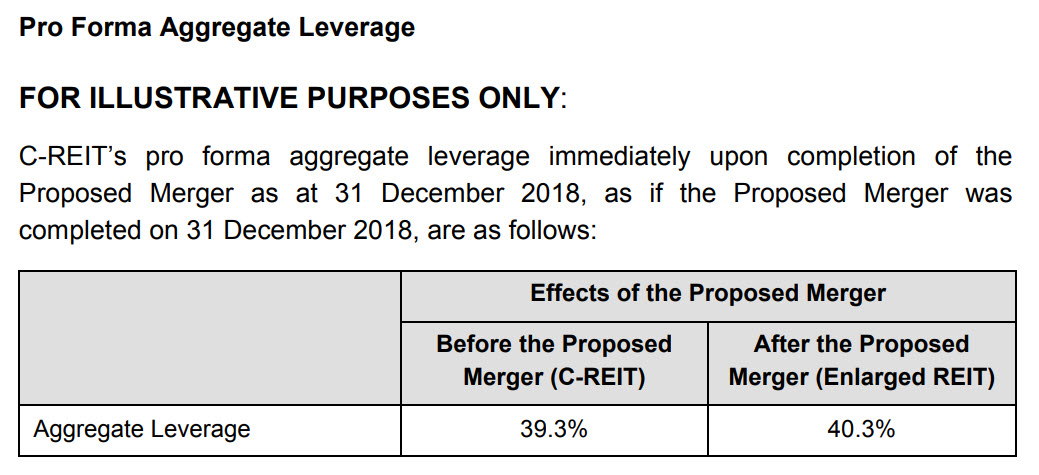

- Increase in gearing/leverage

- Potential decrease in price because OUE Commercial REIT has almost never traded near book value/NAV. Using the pro forma NAV of $0.62 and assuming it trades around 0.8 PB (giving it a little premium due to larger and more diversified assets base), the share price will be around $0.496

Having said that, if you think otherwise and believe that the price of OUE Commercial REIT will increase after the merger. Then there exists an opportunity for you to arbitrage by buying OUE Hospitality Trust share. You can use this spreadsheet for your analysis - Merger of OUE Commercial REIT & OUE Hospitality Trust

We will be staying away. Hope this short analysis will help all the current/future shareholders!

Do like any of the following for the latest update/post!

1. FB Page - KPO and CZM

2. Twitter - KPO and CZM

3. Click here to subscribe using email :)

4. Instagram - KPO_and_CZM (Did you see those delicious food photos to the right --> Unfortunately, you can't see it on mobile.)

OUE Hospitality Trust shareholders will be receiving $0.04075 cash + 1.3583 new OUE Commercial REIT shares for every existing OUE Hospitality Trust share. Let's look at the numbers to see why I deemed it as a bad deal.

OUE Hospitality Trust (Before Merger)

|

| Numbers from OUE Hospitality Trust 2018 Annual Report |

NAV: $0.75

PB: 0.980

DPU: 0.0499

Dividend Yield: 6.79%

OUE Commercial REIT (Before Merger)

Last Close: $0.52

NAV: $0.71

PB: 0.732

DPU: 0.0348

Dividend Yield: 6.69%

|

| Pro Forma DPU |

|

| Pro Forma NAV |

|

| Pro Forma Aggregate Leverage |

Issue Price: $0.57

NAV: $0.62

PB: 0.919

DPU: 0.0348

Dividend Yield: 6.11%

What this means for OUE Hospitality Trust shareholders:

- The "buyout" is at below book value/NAV

- You got diluted/the dividend yield drops for the "same" investment

What this means for OUE Commercial REIT shareholders:

- You got diluted big time as the NAV decreases by ~12.7%

- The pro forma DPU shows an increase of 0.0341 to 0.0348 but 0.0341 is not the actual DPU for FY 2018. Unable to determine if it is truly yield accretive as stated

- Increase in gearing/leverage

- Potential decrease in price because OUE Commercial REIT has almost never traded near book value/NAV. Using the pro forma NAV of $0.62 and assuming it trades around 0.8 PB (giving it a little premium due to larger and more diversified assets base), the share price will be around $0.496

Having said that, if you think otherwise and believe that the price of OUE Commercial REIT will increase after the merger. Then there exists an opportunity for you to arbitrage by buying OUE Hospitality Trust share. You can use this spreadsheet for your analysis - Merger of OUE Commercial REIT & OUE Hospitality Trust

We will be staying away. Hope this short analysis will help all the current/future shareholders!

Do like any of the following for the latest update/post!

1. FB Page - KPO and CZM

2. Twitter - KPO and CZM

3. Click here to subscribe using email :)

4. Instagram - KPO_and_CZM (Did you see those delicious food photos to the right --> Unfortunately, you can't see it on mobile.)

I do not understand the issue price of $0.57 per new OUE Commercial REIT share. Where does this number come from and how can it be applied/enforced?

ReplyDeleteSurely the H-REIT unitholders will receive newly issued C-REIT units according to the offer. That's it.

The market will determine the price once the units are traded on SGX.

The current price of C-REIT is S$0.505, way below the S$0.57.

Hi RP,

DeleteIt is in their announcement - https://links.sgx.com/FileOpen/OUECT_Acquisition_Announcement.ashx?App=Announcement&FileID=550713

Alternatively, I captured it in one of my screenshot too. Looked at "Pro Forma DPU/NAV" notes...

Please do not get confused by the current price and the illustrative issue price.

Further to the last comment.

ReplyDeleteAssuming the S$0.57 price is only an example, then the numbers

Issue Price: $0.57

NAV: $0.62

PB: 0.919

DPU: 0.0348

Dividend Yield: 6.11%

using the latest close become

Issue Price: $0.505

NAV: $0.62

PB: 0.815

DPU: 0.0348

Dividend Yield: 6.89%

Which looks a lot better for both the C's and the H's....

There are another few months to play out yet.

It is not so straightforward. Both the acquisition fee and the shares paid out to the H's shareholders are illustrated using $0.57. If the current price is $0.505 now, why should the deal still be based on $0.57 numbers?? So is there a need to issue more shares as fees or to H's shareholders? That also means further dilution right?

DeleteAnyway, you got to wait till the voting goes through or the deal is confirm to get the final numbers and it is just a bad deal in general...

Hi,

ReplyDeleteI am not sure about the shares to be issued as fees, I find that confusing. Is the fee set in S$ or in units?

But the exchange ratio for H-REIT units is now fixed. They will not change that.

These votes pretty much always go through, and this merger doesn't seem to be such a bad deal.

Indeed, if the price of H-REIT drops further I might even add to my holding.

payment is pay part by units and cash. No. of units to be paid depends on the share price. And the price is higher probable to be lower rather that higher.

DeleteI would say this merger is slightly better than the Downtown acquisition. But most impt is the manager/sponsor does not care its shareholder's interest with bad deals. A merger of hospitality, office ad retail remains to be seen if it performs. If you have hold this reit since IPO, you are coughing out more $ then dividends.

DeleteIf you think it is a good deal. compare it or the reit performance to other reit, it is badly managed

The exchange rate to change with OUEHT has not been finalize until EGM has been voted. 57cent is just example as all pro forma is usually stated for a feel of the trasnsactions

Please read the edge writing if you are interested

https://www.investingnote.com/posts/1363397

Haha. I agree with what Layers said...

Delete@RP, if you think it is a good/attractive investment, by all means add to your holding. At the end of the day, you make your own investment decision :)

ESR Reit has not been trading near it's NTA before merger with Viva. ESR Reit was trading at around 50 cents with NTA of around 59 cents. After merger, ESR is now trading above it's NTA, trading price of 53 cents vs NTA of 47 cents. So OUE C reit should rise to at least 55 cents due to it's bigger size and ranking among one of the biggest s-reits.

ReplyDeleteHaha. Notice how you said "should" rise to at least 55 cents... That's the market right. Unpredictable. At the end of the day, what matters is if one makes money out of it :)

Delete