This month has been a pretty busy month and KPO will be on reservist for the next 2 weeks! CZM has finally come back to blog about our 9th year anniversary lunch at JAAN. Do check it out and show your support :)

There was an interesting discussion going on in the comments section of my last article - Who has the lowest fees? StashAway vs Smartly vs AutoWealth. It all started when foolish chameleon asked if one should be switching the money from one robo advisor to another once one has reached the next level to be entitled to lower fees. The followings were the conclusion:

- StashAway: < $10,000 or > $400,000

- AutoWealth: between $10,000 and $100,000

- Smartly: between $100,000 and $400,000.

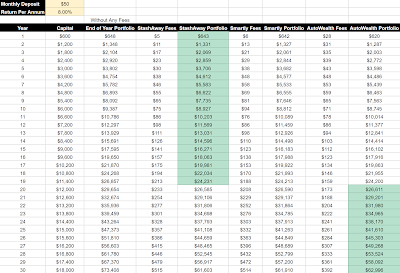

As usual, KPO spent some time and played with the numbers to find out how would the difference in fees affect the growth of one's portfolio. For simplicity, one assumption is made - the 3 robo-advisors provide the same annual returns.

Interestingly, the results turned out to be quite different from my previous article. The previous article was a one dimensional analysis on the fees based on the absolute amount of the portfolio. This time round, the compounding effect was added to provide a two dimensional analysis.

Scenario 1: Invest $50 on a monthly basis and the expected returns were 7% per year.

Scenario 2: Invest $50 on a monthly basis and the expected returns were 8% per year.

Scenario 3: Invest $500 on a monthly basis and the expected returns were 7% per year.

Scenario 4: Invest $1,000 on a monthly basis and the expected returns were 7% per year.

If we are choosing a robo advisor purely from a fee/cost perspective, AutoWealth seems to be the most cost-effective after taking into account the compounding effect. On the other hand, I hardly see Smartly performing better. I would recommend that you download a copy of this google spreadsheet and play with the numbers yourself. Simply change the number in the highlighted cells, everything else is formula linked.

However, I would like to point out that the above assumption is too simple. lol. The 3 robo-advisors will definitely provide different returns. CNBC has published an article on it - Returns vary widely for robo-advisors with similar risk. Another article by Senzu also shows the difference in returns - Compare Performance & Portfolios of Robo Advisors. This is because the asset allocation, the underlying ETFs as well as the way the logic/algorithm use to rebalance the portfolio will all be different.

Will we continue to use StashAway? Yes! Among the 3 robo-advisors, only StashAway provided a clear explanation of their logic/asset allocation framework - ERAA (Economic Regime-based Asset Allocation). On the other hand, AutoWealth "takes a rule-based approach towards investing" but I could not find any further information (the same can be said for Smartly).

Update: As pointed out by Kevin, Smartly uses Harry Markowitz Modern Portfolio Theory which you can find out more through Investopedia - Harry Markowitz. Miru also shared his own experience dealing with the 3 robo-advisors in the comment section. Once again, the cost/fee should not be the only consideration.

Hope you enjoy the article!

StashAway Referral Link for Our Readers

Here you go: KPO and CZM Referral Link

Do like any of the following for the latest update/post!

1. FB Page - KPO and CZM

2. Twitter - KPO and CZM

3. Click here to subscribe using email :)

There was an interesting discussion going on in the comments section of my last article - Who has the lowest fees? StashAway vs Smartly vs AutoWealth. It all started when foolish chameleon asked if one should be switching the money from one robo advisor to another once one has reached the next level to be entitled to lower fees. The followings were the conclusion:

- StashAway: < $10,000 or > $400,000

- AutoWealth: between $10,000 and $100,000

- Smartly: between $100,000 and $400,000.

As usual, KPO spent some time and played with the numbers to find out how would the difference in fees affect the growth of one's portfolio. For simplicity, one assumption is made - the 3 robo-advisors provide the same annual returns.

Interestingly, the results turned out to be quite different from my previous article. The previous article was a one dimensional analysis on the fees based on the absolute amount of the portfolio. This time round, the compounding effect was added to provide a two dimensional analysis.

Scenario 1: Invest $50 on a monthly basis and the expected returns were 7% per year.

Scenario 2: Invest $50 on a monthly basis and the expected returns were 8% per year.

Scenario 3: Invest $500 on a monthly basis and the expected returns were 7% per year.

Scenario 4: Invest $1,000 on a monthly basis and the expected returns were 7% per year.

If we are choosing a robo advisor purely from a fee/cost perspective, AutoWealth seems to be the most cost-effective after taking into account the compounding effect. On the other hand, I hardly see Smartly performing better. I would recommend that you download a copy of this google spreadsheet and play with the numbers yourself. Simply change the number in the highlighted cells, everything else is formula linked.

However, I would like to point out that the above assumption is too simple. lol. The 3 robo-advisors will definitely provide different returns. CNBC has published an article on it - Returns vary widely for robo-advisors with similar risk. Another article by Senzu also shows the difference in returns - Compare Performance & Portfolios of Robo Advisors. This is because the asset allocation, the underlying ETFs as well as the way the logic/algorithm use to rebalance the portfolio will all be different.

Will we continue to use StashAway? Yes! Among the 3 robo-advisors, only StashAway provided a clear explanation of their logic/asset allocation framework - ERAA (Economic Regime-based Asset Allocation). On the other hand, AutoWealth "takes a rule-based approach towards investing" but I could not find any further information (

Update: As pointed out by Kevin, Smartly uses Harry Markowitz Modern Portfolio Theory which you can find out more through Investopedia - Harry Markowitz. Miru also shared his own experience dealing with the 3 robo-advisors in the comment section. Once again, the cost/fee should not be the only consideration.

Hope you enjoy the article!

StashAway Referral Link for Our Readers

Here you go: KPO and CZM Referral Link

Do like any of the following for the latest update/post!

1. FB Page - KPO and CZM

2. Twitter - KPO and CZM

3. Click here to subscribe using email :)

Hi KPO!

ReplyDeleteNice to see more and more attention on robo-advisors. Smartly uses "Harry Markowitz Modern Portfolio Theory to minimize the risk of your investments." It's listed on their website main page ;)

Kevin

Hi Kevin,

DeleteThanks for pointing that out! I totally missed it digging high and low in their FAQ and blog, turns out it was stated in the main page @_@

Hi KPO. Thanks for working on the numbers!

ReplyDeleteDo you consider another cost factor: the forex conversion fee. StashAway: 0.1%. Auto-wealth: 0.5%. Smartly: no reply from their customer service. How will this affect the total cost?

My other findings from poking around SA & AW:

* AW portfolio is very simple (close to Bogleheads) whereas SA has wider ETF in their portfolio.

* SA allows partial unit (omnibus account). AW will only buy/sell whole unit.

* To open an account with AW, you need to meet up with their rep in person and processing takes 1 week. SA is fully online and activated immediately.

* SA: email response is very fast. AW: whatsapp response is pretty fast too. It's too bad Smartly did not reply my email despite follow-up.

--Miru

Hi Miru,

DeleteThanks for sharing your experience here! One thing I really like about SA is the partial unit feature as well. Unfortunately, I did not take FX into account. It would be a lot more complicated to do that. lol.

Based on my own experience, SA has been pretty responsive and the onboarding process was pretty smooth.

ahh, thanks for that KPO.

ReplyDeletei guess the results is not unexpected.

no one knows for sure what their returns will be; past performance is not a measure of future returns.

i guess the only way is to plonk down $X in each of the platform.

blogger Finance Smith has both account in SA and S. something you can compare with.

Hi foolish chameleon,

DeleteYou are right! No way to know/measure.

I know he's doing it! So far I have only seen both of us putting our monies in or blogging about it. Anyway, let him test the water for everyone. Hahahaha.

Hello thanks for the analysis! SA also has a 0.15 to 0.25 pct in fees for ETFs. This is also a push factor =)

ReplyDeleteHi myles,

DeleteI am guessing you are referring to the expense ratio for each and individual ETF. That is applicable for all ETF and is transparent to us. Even STI ETF has it too.