After investing for slightly more than 6 months in Syfe REIT+, I am pleased with the way they are handling the corporate actions. They are definitely more transparent as compared to a REIT ETF where you will be able to see all the corporate actions such as mergers, rights issues, etc. in your transactions. Let me show you some snippets:

|

| Corporate actions for CMT and CCT merger/combination |

|

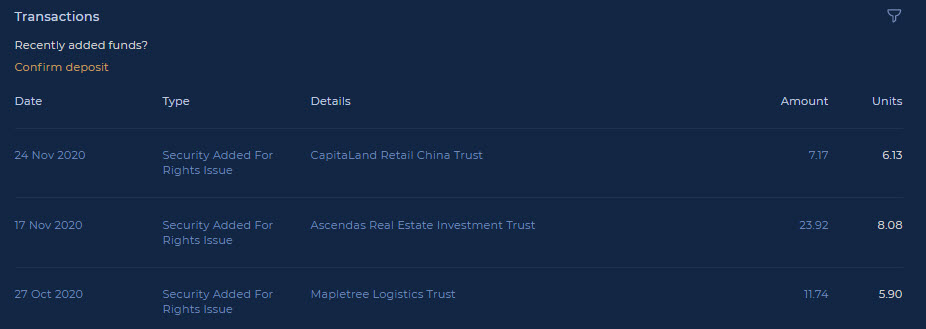

| Various Rights Issues |

This is really a fuss free way to invest in REITs. Simply DCA on a monthly basis and you do not even have to trouble yourself with the corporate actions. The one and only thing about Syfe which really annoys me is the inaccuracy in the units being displayed both in the transactions and the portfolio composition (to 2 decimal places). Having said that, I am aware that behind the scene, they are actually tracking them to 6 decimal places. A simple UI change should fix the issue but I am not sure why is it not in their priority ¯\_(ツ)_/¯

Our Syfe Portfolio

Composition: 100% REITs

Dividend: Reinvest

Monthly Investment: $1,000

Composition: 100% Equities

Dividend: Reinvest

Monthly Investment: $500

Account Statement (Lifetime)

Our current tier is Blue (<$20,000). This is determined by the size of the portfolio (currently $11,255.26) which in turn determines the fees to be charged. The statement lifetime return is $1,555.26 which includes a $1,220 referral bonus. The actual lifetime return would be $335.26. Thanks to our readers for using our code!

Account Statement (November 2020)

Account Statement (November 2020)

The return for the month is $725.97 which includes a $20 referral bonus. This means our actual return for the month is $705.97.

As of 19 December 2020, this is our portfolio performance:

As of 19 December 2020, this is our portfolio performance:

Capital: $7,500.00

Current: $8,842.63 (21.09% - return is skewed due to referrals)

Current: $8,842.63 (21.09% - return is skewed due to referrals)

Capital: $2,700.00

Current: $3,259.07 (39.90% - return is skewed due to referrals)

Current: $3,259.07 (39.90% - return is skewed due to referrals)

Transaction Breakdown

There are too many so I will just share a snippet. Anyway, if you want to extract the transaction information from Syfe, do take a look at this article - Syfe Transactions Parser. Anyway, the parser will not work for the Equity100 and Global ARI portfolio when there are small transactions (<0.01). You can refer to this for more information - Syfe - July 2020. The parser will work if Syfe is willing to change its UI and display more decimal places...

|

| REIT+ |

|

| Equity100 |

After parsing them into a csv file, I pivoted the data to get the following view.

Management Fee

The management fee can be obtained by $9,971.44 x 0.65% / 366 * 30 ~ $5.28.

StocksCafe

In my opinion, the return captured by StocksCafe will be a more accurate representation of our portfolio return as the referral bonuses are treated as capital. Having said that, I can also understand why Syfe treats them as a return instead of a deposit too. Just a different perspective.

StocksCafe

In my opinion, the return captured by StocksCafe will be a more accurate representation of our portfolio return as the referral bonuses are treated as capital. Having said that, I can also understand why Syfe treats them as a return instead of a deposit too. Just a different perspective.

|

| Transactions updated till 30 Oct 2020 |

Anyway, looking at the time-weighted return (17.53%) for this year, we can see that Syfe REIT+ 100% is outperforming STI ETF (including fees) but underperforming when compared against SPY or IWDA. In addition, if we were to look at the projected dividends till the end of the year based on the existing investment, we can expect $141.01 of dividends or $11.75 per month. Since the dividends >> fees, this is a pretty sustainable portfolio assuming if there's no capital loss.

New Syfe customers will have their first $30,000 managed free for 6 months when they use our new referral code (KPOCZM). We will be receiving a $10 cash incentive for our portfolio if you invest $500 or more.

If you are interested in the smart portfolio tracker (StocksCafe) which I am using as shown above, sign up using my link for a longer trial period :) Refer to our Referrals page for more information.

You might be interested in previous months update too:

- Syfe REIT+ (100%) Review

- Syfe - May 2020 - $1,135.43

- Syfe - June 2020 - $2,558.58

- Syfe - July 2020 - $3,872.68

- Syfe - August 2020 - $6,260.30

- Syfe - September 2020 - $8,019.86

New Syfe customers will have their first $30,000 managed free for 6 months when they use our new referral code (KPOCZM). We will be receiving a $10 cash incentive for our portfolio if you invest $500 or more.

If you are interested in the smart portfolio tracker (StocksCafe) which I am using as shown above, sign up using my link for a longer trial period :) Refer to our Referrals page for more information.

You might be interested in previous months update too:

- Syfe REIT+ (100%) Review

- Syfe - May 2020 - $1,135.43

- Syfe - June 2020 - $2,558.58

- Syfe - July 2020 - $3,872.68

- Syfe - August 2020 - $6,260.30

- Syfe - September 2020 - $8,019.86

- Syfe - October 2020 - $9,029.29

- Syfe - November 2020 - $11,255.26

Do like any of the following for the latest update/post!

1. FB Page - KPO and CZM

2. Twitter - KPO and CZM

3. Click here to subscribe using email :)

4. Instagram - KPO_and_CZM (Did you see those delicious food photos to the right --> Unfortunately, you can't see it on mobile.)

Do like any of the following for the latest update/post!

1. FB Page - KPO and CZM

2. Twitter - KPO and CZM

3. Click here to subscribe using email :)

4. Instagram - KPO_and_CZM (Did you see those delicious food photos to the right --> Unfortunately, you can't see it on mobile.)